|

|

|

Professional Partnerships: Hospice Philanthropy Group L.L.C.

|

Quickie quiz:.....86% of Americans can't answer a simple 10 question finance quiz, can you? Link below Senior Spirit.....Click the Senior Spirit link (below left) for a copy of the latest articles from Certified Senior Advisors Past issues of the Newsletter are available in the Newsletter Archives To subscribe to this newsletter E-mail and put Subscribe in the subject line. Join me..... at the 2016 Crescendo Practical Planned Gift conference on September 26th Chicago and hear a presentation on "Building a Professional Advisory Committee" _____________________________________________________________________ |

|---|---|

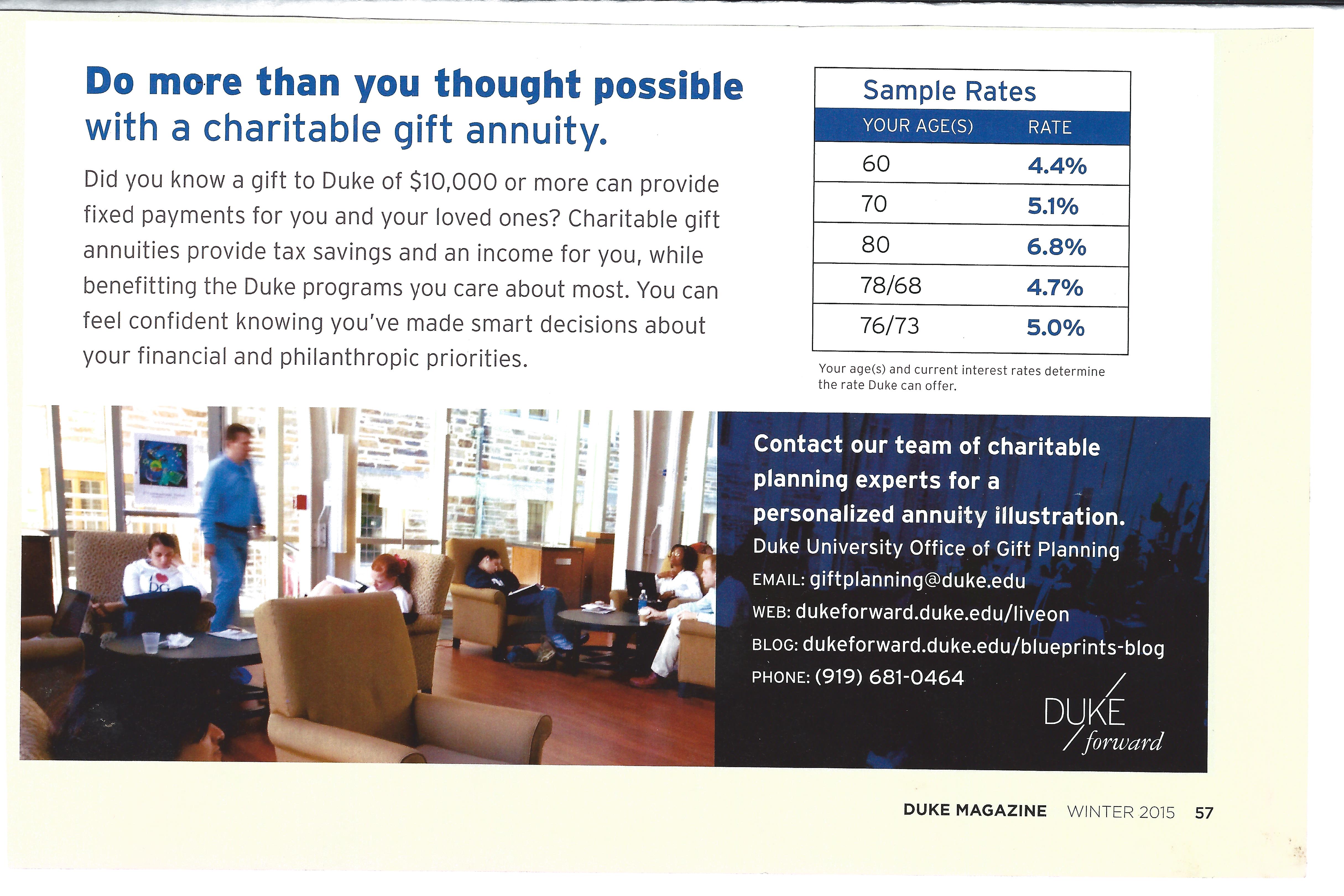

The Legacy IRA Act was introduced on May 6th by House Ways and Means Committee. Current law: Individuals age 70 ½ or older can make direct (outright) gifts from an IRA of up to $100,000 per year to public charities (other than donor advised funds and supporting organizations) and to private operating and pass-through (conduit) foundations without having to report the IRA distributions as taxable income on their federal income tax returns. Although a charitable deduction is not allowable, not being taxed on otherwise taxable income is the equivalent of a charitable deduction. First enacted in 2006, this law was made permanent by the PATH Act of 2015. Direct IRA rollovers have helped American charities feed the hungry as well as provide education, medical services, housing assistance and myriad other services that Americans need. Legacy IRA bill: The expansion in the Legacy IRA bill authorizes tax-free IRA rollovers for gifts that benefit charities and provide taxable retirement income—charitable life-income plans—for the donors. At the donor’s death, the assets in the plan are owned outright by the qualified charity. Charitable deductions aren’t allowable for amounts transferred to the life-income plans (charitable remainder trusts and charitable gift annuities). But not being taxed on otherwise taxable income is the equivalent of a charitable deduction. Qualified charities: The same donees authorized for direct outright transfers to charities. Annual ceiling on transfers: It’s $400,000, for individuals 65 or older. For individuals 70½ or older, the combined ceiling for direct and life-income transfers from their IRAs is $400,000, with a $100,000 cap for direct transfers. Minimal revenue cost to the government: Under the authorized life-income plans, the IRA owners will be taxed on income received at ordinary income tax rates. Because the payouts are 5 percent or more, there generally will be more income paid from the charitable life-income plans than under the normal required minimum distribution (RMD) rules. The only authorized income beneficiaries of the life-income plans are the individual IRA owner, his spouse or both. At death, the assets in the plan go directly to the named qualified charity or charities and not to family members. Why wouldn’t IRA owners just give outright to charity (direct gifts) from their IRAs as provided under the now permanent law? Many IRA owners want to make charitable gifts, but also need retirement income. The life-income IRA rollover is a way for donors of average resources to combine charitable gifts with retirement income. Many charities have donors “standing by” to make life-income charitable gifts from their IRAs. This is a middle class charitable IRA rollover. It allows average Americans (who meet the minimum age requirement) to benefit charities. Four-year trial: The law wouldn't’t be permanent but would last for a four-year trial period. That provides adequate time to determine the expansion’s efficacy. Cost: The bill’s cost is $106 million over 10 years. This is a small fraction of the money that charities will receive as a result of enactment. Common Questions and Answers: Here are some common questions that practitioners have expressed about the Legacy IRA Act and my answers. Minimum payout - Q. Why is the minimum payout of the life-income plans 5 percent? A. The minimum 5 percent payout for unitrusts and annuity trusts in the bill has nothing directly to do with the bill. The law has required the 5 percent minimum since 1969, when unitrusts and annuity trusts were first authorized. The minimum payout for gift annuities in the bill is 5 percent, and gift annuity laws don’t require that minimum. It’s important, however, that the 5 percent minimum in the Legacy IRA Act be for gift annuities, as well as unitrusts and annuity trusts. Reason: The bill was favorably scored (the cost to the Treasury) by the Joint Committee on Taxation based on a 5 percent minimum payout for all three life-income plans. That generally is at least as much as would be required under the RMD rules for IRAs. Thus, the government won’t lose tax dollars if payments are made from the charitable IRA rather than the original IRA. Caution for life-income IRA gift annuities: A charity should follow the rates that it offers for the usual gift annuities. If 5 percent is greater than the usual rate, the charity shouldn't enter into an IRA life-income charitable rollover. Pooled income funds - Q. Why aren’t pooled income funds included in the bill? A. Many pooled income funds earn less than 5 percent. Those funds are allowed to only pay income (and can’t pay out principal to make a 5 percent payment). Assignability of legacy IRA - Q. Why can’t a legacy IRA be assigned to the named charitable remainder organization? A 1. Policy. In dealings with Congress over many years on the life-income charitable IRA, strong concerns have been expressed on the issue of assignability. If a donor can assign his charitable IRA, it’s possible that the donor won’t have sufficient retirement income and might have to turn to the government. A 2. Fiscal. The payments from the charitable life-income rollover will be fully taxable as ordinary income. If the donor assigns his income interest in a life-income charitable rollover to a charity, the government wouldn’t get taxable income from the charity as it would if the donor continues to receive the life-income rollover payments. Also the donor could, in effect, increase the current $100,000 ceiling for direct rollovers to $400,000 each year. These issues have come up over the years and most recently in meetings with the staff of the Joint Committee on Taxation. A favorable score (cost to the government) of the bill of only $106 million over 10 years wouldn’t have been obtained if the life-income IRA beneficiaries could assign their interests to charities. If so assigned, the government would lose taxes on the income because charities are tax- exempt. The score could have been in the billions, rather than $106 million over 10 years. __________________________________________________________________________________ Also note McLeodFoundation has PDF links to their previous publications by issue date: Annual Reports, Foundation Newsletter, Legacy Series Newsletters and Foundation Donors lists by giving level are all available online. Marketing Idea #2.....Every newsletter should have an advertisement or article on a legacy gift option or strategy. For two examples from Duke University from their major publication "Duke Magazine." Click Example #1 and Example #2. Example #1 includes a personal testimonial on the benefits of gift strategies. Example #2 promotes charitable gift annuities. Note: the five ways you can contact the Office of Gift Planning - Email, Web, Blog and phone. Do your ads include multiple contact methods? _____________________________________________________________________________________________________ ___________________________________________________________________________________________________ |

|

Gift Annuity Rate Update and Laminated Gift Annuity Rate Charts..... At its semiannual meeting on April 5, 2016, the Board of Directors of the American Council on Gift Annuities (ACGA) reaffirmed the existing schedule of suggested maximum rates for charitable gift annuities which was originally published on January 1, 2012. As part of its ongoing review process, the Rates Committee of the ACGA monitors on a weekly basis certain interest rates that underlie the investment return assumptions used to create the rate schedules. The committee also evaluates annuitant mortality and other assumptions as appropriate. The ACGA uses the mortality assumptions from the 2012 IAR Mortality Table recently promulgated by the National Association of Insurance Commissioners when calculating a schedule of suggested gift annuity rates. The ACGA will meet again in April, 2016. Rate Chart....... If you would like a laminated rate chart for the most recent rates simply request one using the following E-mail request and put Laminated Chart in the subject line. Download a PDF chart of single life $10,000 cash gift and two-life $100,000 security gift for ages 60,65,70,75,80 here. ______________________________________________________________________________________________________ Charitable Trust Review?.....For a quick review of Charitable Trusts check out the following guide that is being distributed to financial professionals "Giving Today to Guarantee Tomorrow: A Charitable Trust Review." While the guide was developed for professional advisors and agents, it is an excellent review of various charitable trust techniques. __________________________________________________________________________________________ IRA Rollover Successes.....Recently a Blog Post and CresNotes a publication of Crescendo Interactive released results of their clients marketing efforts for IRA Rollover gifts. The top performing subject lines for email blasts were: The IRA Rollover is Back;, Congress Passes Bill and Makes the IRA Rollover into Law!; IRA Charitable Rollover Permanent!; and IRA Rollover Passed. Some results were: Michigan Technological University received $427,992 from 30 IRA gifts, with 12 gifts of $10,000 or more. University of North Carolina at Chapel Hill reported $1,031,905 in rollover gifts. With the IRA Rollover option now permanent promotion of this new gift technique needs to be done throughout the year. ___________________________________________________________________________________________ Quiz Answer.....Link to financial quiz _________________________________________________________________________________________ Understanding the Reasons for Giving Key to Strategic Philanthropy?.....Bruce DeBoskey's recent article in the Denver Post business sections outlined for advisors the basic motivations of probable donors. As advisers to philanthropists, we have learned that there are many motivations for parting with hard-earned money in pursuit of a greater good. There is no "bad" reason to be philanthropic. The wide range of reasons we encounter include: Gratitude, Religion or faith, Ego and recognition, Healing or strengthening family bonds, Passing values to rising generations, Guilt, Compassion, Prevention of similar experiences, Access and power, Creating a legacy, Connection and well-being, and Tax savings. ________________________________________________________________________________________ News and Notes....TAXES - 90% of American taxpayers pay more in payroll taxes (that support Social Security, Medicare and unemployment benefits) than they pay in federal income tax (source: Peter G. Peterson Foundation) NO FANCY DEGREE - 20 current members of the House of Representatives (out of 435 members in the House) have no educational degree beyond a high school diploma (source: Congressional Research Service) TAX DATA - The top one-tenth of 1% of US taxpayers (based upon adjusted gross income) paid more federal income tax ($228 billion) during tax year 2013 (the latest year that tax information has been released) than the federal income tax ($169 billion) paid by the bottom 75% of taxpayers (source: Internal Revenue Service) JUST TAKES LONGER TODAY - 25 years ago (1991), 89% of American workers expected to be retired by at least age 65. Today (2016), only 57% of American workers expect to be retired by at least age 65 (source: Employee Benefit Research Institute) SHORT OF CASH - Only 1 in 7 (14%) American workers have accumulated savings and investments (both pre-tax and post-tax combined) of at least $250,000, not counting the value of the worker’s primary residence or the present value of any pension plan he/she has earned (source: Employee Benefit Retirement Institute). CAN’T GET AHEAD - 45% of the 118 million households in the United States live “paycheck-to-paycheck” (source: National Endowment for Financial Education). (NOT PLANNED GIFT PROSPECTS) According to the 2015 Aegon Retirement Readiness Survey, only 14% of working Americans over age 55 plan to retire before reaching 65, and 53% of people over age 55 plan to work at least part-time during retirement. ______________________________________________________________________________________________________ |

|

Kudos Corner - Celebrating gifts of all types and sizes In this section I periodically highlight some recent gift expectancies and gift program elements I think will be helpful and informative, not all gifts are included. Stop back next month for a gift update. _____________________________________________________________________ |

|

James E. Connell and Associates is a national consulting service devoted to increasing resources for charities using the power of charitable estate and gift planning techniques. Pinehurst

office: PO Box 3335, Pinehurst, NC 28374 |

|

To subscribe

from this newsletter click this link

and in the title line put subscribe |

|

Quotes

for today

Quotes

for today IRA Life Income.....A life-income charitable individual

retirement account rollover bill (HR5171) adapted

from information in

IRA Life Income.....A life-income charitable individual

retirement account rollover bill (HR5171) adapted

from information in  Marketing

Idea #1.....Salute

your Legacy Society with full pages in you annual Annual Report, don't

make them an afterthought.

Marketing

Idea #1.....Salute

your Legacy Society with full pages in you annual Annual Report, don't

make them an afterthought. {kind=link}

{kind=link}